Crypto Market Fit: Redefining Product Market fit in web3

Since the beginning of the consumer internet, investors and builders have regarded Product Market Fit (PMF) as the north star for any startup. A startup isn’t actually a company until they find PMF. Instead, they are a founding team who are hypothesis testing and proving a set of assumptions to be true.

Before finding PMF, founders are lab scientists preparing, testing, and evaluating new reagents and controls. After finding PMF, these scientists masked in Warby Parkers graduate from the lab and are immortalized as real entrepreneurs, upon which they enter the pearly founder gates of Silicon Valley.

But PMF is not a single victory; it’s a constant war. Once you win the first PMF battle, competition will arrive and you will be battle tested every day. Your competition dreams of unseating you from your PMF throne and finding victory at your expense — or so this was the war that we fought in web2.

In 2021, the term “web3” became part of internet vernacular. The decentralization ethos and community focus suggested that finding PMF through your actual product was just a small part of the early stage founder journey. We were introduced to new growth levers including tokens, airdrops, and DAOs with composability and ownership at their core.

Many of the most successful projects in crypto have had very low usage in terms of how we define success metrics in web2. As an investor and builder, I’ve had to ask myself what PMF actually means in crypto, and consider whether the term itself is outdated and requires a new definition for crypto products.

I’ve staked my career and our entire venture fund on crypto finding mainstream adoption. But I often question whether mainstream adoption is actually required for the space to achieve its mission, and for founders and investors to succeed. My belief is that we need a new success metric for the space altogether: Crypto Market Fit.

Crypto Market Fit (CMF) is PMF for web3-native products judged by web3 metrics and mechanics rather than web2’s old standards.

The structure of a language determines a speaker's perception and categorization of an experience. Because web3 is a new experience, we sometimes need to make up a few terms here and there.

Apples and Oranges: Web2 v Web3 Metrics

Coming from a web2 product background at Tinder, my framework for PMF was attached to very specific metrics focused on consumer software. At Tinder, our dashboards were designed for us to think of our users as representations of DAU/WAU/MAU. We thought about our top-of-the-funnel in D1/D7/D30 methodology.

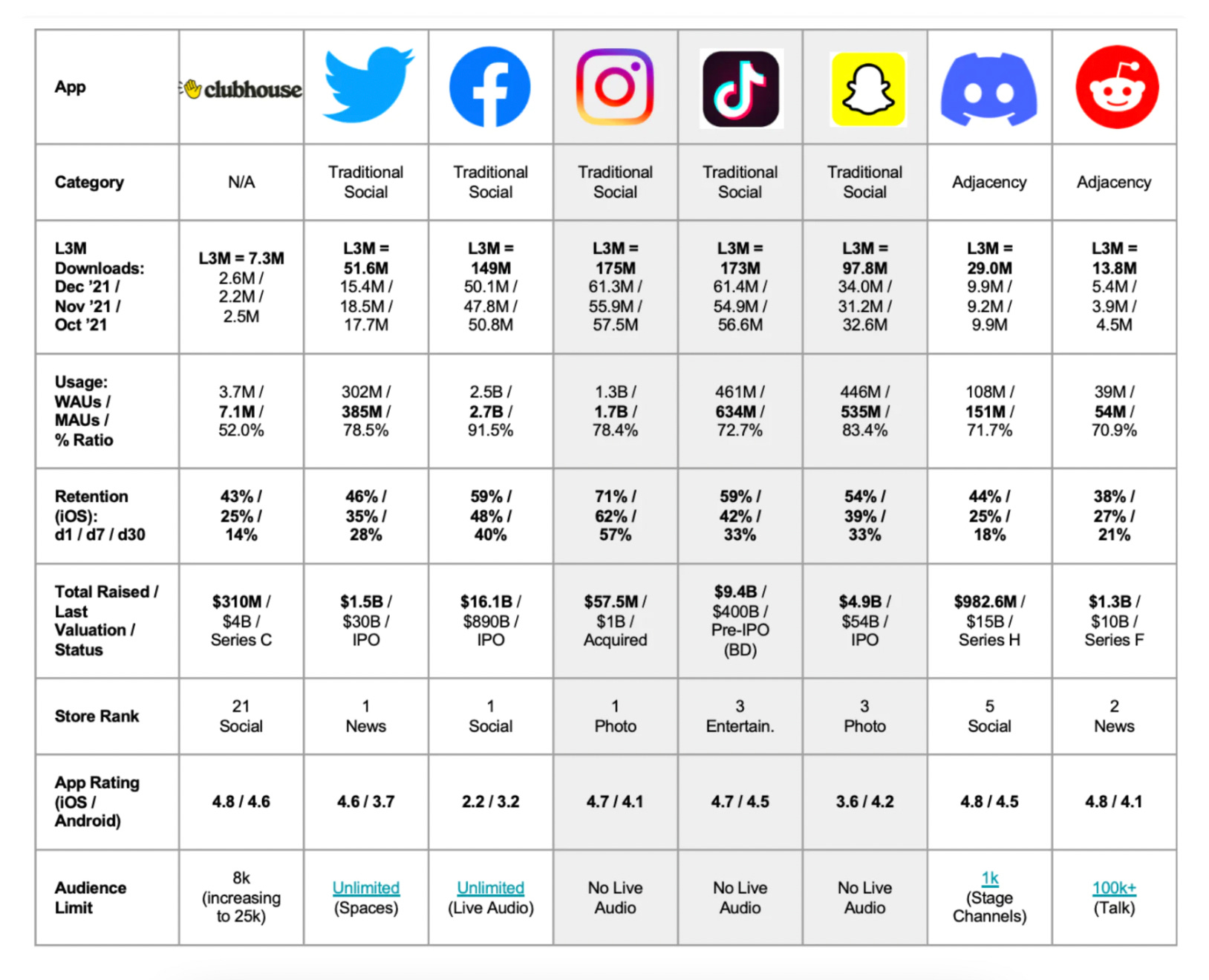

If our business metrics dropped overnight, the Tinder fire alarms rang (or at least our pagers buzzed). We would race to sit in crowded conference rooms with engineers for debugging sessions, like real-life firefighters putting out a raging summer blaze. We were trained to look at graphs like the one below and compare our own metrics:

A quick glance at the above graph and you’ll see that most of the web2 social products that hit PMF have a WAU/MAU ratio that exceeds 70%. But Uniswap isn’t a consumer social app like Tinder. Many of the best examples of PMF in web3 are highly financialized use cases, which have completely different engagement patterns than swiping right on Tinder or scrolling through Instagram.

Uniswap will never have the DAU of Tinder and it shouldn’t be expected to.

Crypto protocols are not social networks. But industry pundits are still very critical of user base populations sizes within crypto.

There is a new breed of influencers who have built large followings by questioning whether crypto has any legitimate use cases, largely because they see smaller DAU/WAU/MAU numbers and assume there is no value creation or utility. Look at Uniswap financials and you will realize this isn’t the case.

So let’s move away from my home territory of Tinder and look at KPIs for web2 financial consumer apps that undoubtedly display PMF: Coinbase and Robinhood. We’ll compare these to Uniswap, the behemoth DEX that has definitely hit PMF (and maybe CMF).

Because it’s up to companies to choose which statistics they disclose in public filings, it’s impossible to truly standardize this process. Alas, let’s give it a go.

Coinbase Comp:

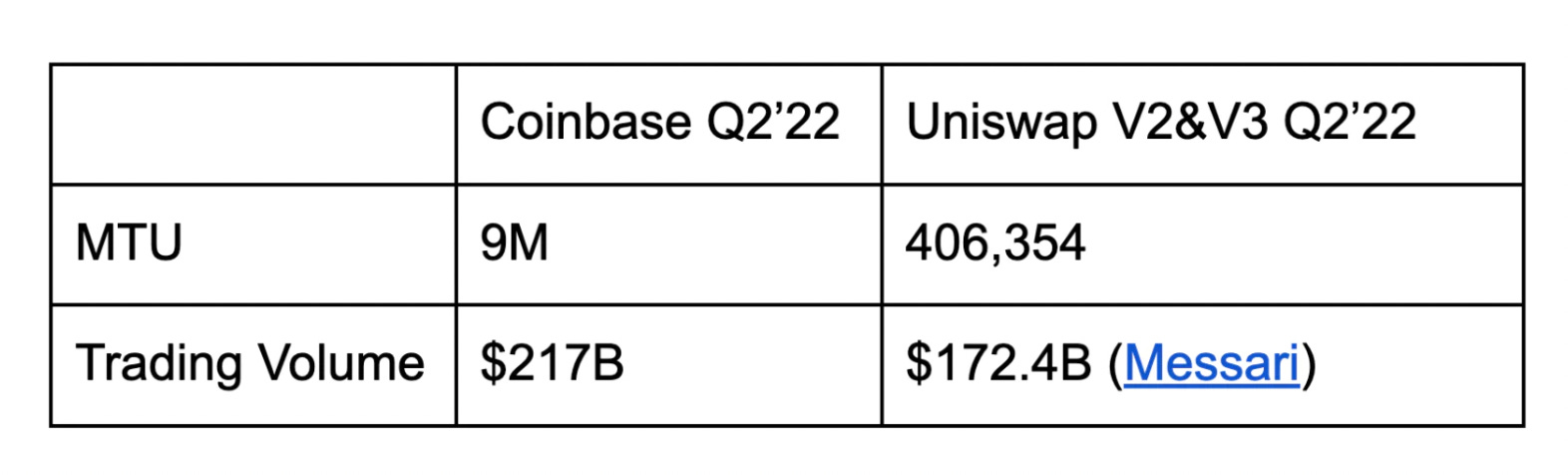

Let’s take a look at MTU (monthly transacting users) and Trading Volume for Coinbase’s Q2 2022 to Uniswap V3 data via msilb7’s Dune dashboard.

With 2.3% of the monthly transacting users of Coinbase, Uniswap did 79% of the trading volume. Mindblowing, right? This is a pattern you’ll begin noticing.

Web3-native financial apps like DEXs can have massive financial success with a fraction of the user-base compared to a web2-native trading platform or even a CEX. Uniswap doesn’t need to do Super Bowl ads to attract millions of users because the whales are already using them.

Perhaps, instead of trying to go for the moon, we should settle for the stars. Yes, it’d be great if web3 achieves full adoption, but let’s be honest - we’re living in web2.5 and we might be here for awhile.

The pushback to this narrative is that much of Uniswap’s DEX trading volume is institutional, whereas Coinbase in largely retail traders.

Point taken, but part of what makes crypto interesting is that the products are accessible to both retail and institutions around the world. This is one of the core value propositions of crypto - creating a more open financial system.

In the long term, a DEX like Uniswap’s mere 208,500 MTU will rise to the millions. Then, what will that trading volume look like?

Robinhood Comp:

Would you rather have quality users or a high quantity of users?

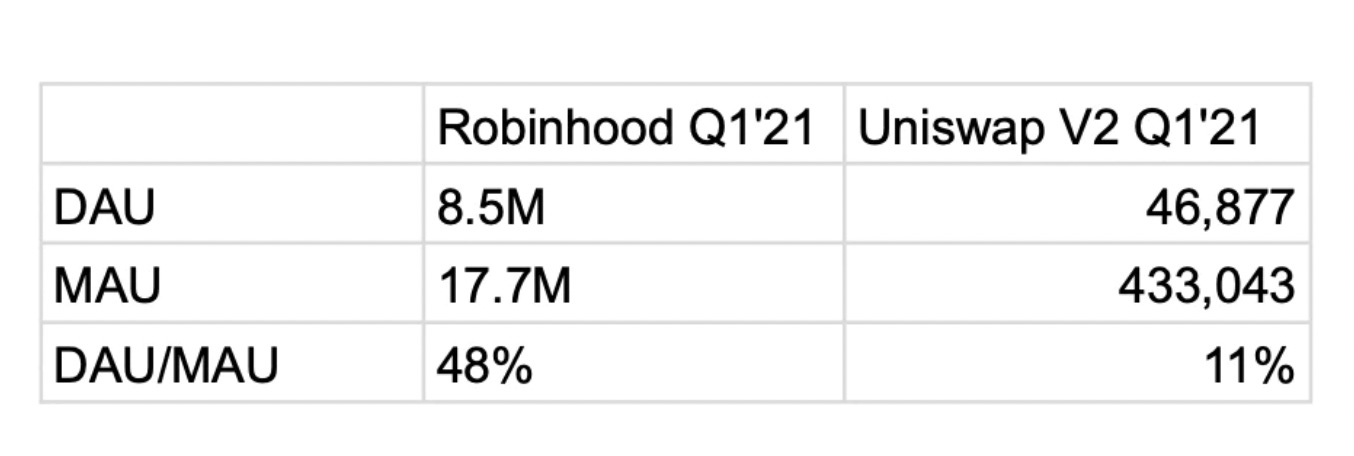

Robinhood hasn’t shared their DAU since Q1 2021 so I’m using that data rather than Q2 2022.

You’re probably saying that Robinhood with a DAU/MAU ratio of 48% has far more PMF than Uniswap with a DAU/MAU ratio of 11%. But this is where the definitions of PMF (Product Market Fit) and CMF (Crypto Market Fit) diverge in web2 and web3.

Robinhood had 8.5M DAU in Q1 2021. Let’s examine what DAU means to Robinhood though. In their Q1 2021 S-1 Form, Robinhood defined DAU as:

A “Daily Active User” is a unique user who makes a debit card transaction, transitions between two different screens on a mobile device while logged into their account or who loads a page in a web browser, at any point during the relevant 24-hour period. A user need not satisfy these conditions on a recurring basis or have a Funded Account to be included in DAU.

Transitions between two screens? Web2 vanity metrics.

Robinhood can get DAU when a user opens their account and swipes around with no transaction. Uniswap’s DAU requires users to swap crypto assets. Web2 product managers created vanity metrics like this and web3 has stripped them away (for now).

So while Uniswap’s numbers are lower, they mean more. Uniswap metrics are based on higher intent actions (i.e. financially interacting with the protocol to perform a financial action). Uniswap, the application, does not yet offer a browsing experience which may increase their DAU/MAU ratio, but let’s look at the data.

Web2 trained our product teams to report DAU/MAU exactly how Robinhood framed their data in their SEC filings. As a product manager, if I can convince a user to tap on a push notification and click between two screens, I have won the earliest part of the DAU/MAU battle.

The product needs to monetize the user at some point, but the product manager is rewarded for moving one very important metric by playing engagement games. In crypto, the metrics are of far higher intent. There is money spent.

Robinhood as a company has a net income (loss) of $1.4B because they have high user acquisition and operational costs with 3900 employees, couple with a low margin business model. Compare this to Uniswap who have reported having 53 employees and and more operational scalability (and undoubtedly better margins) as a decentralized system.

Crypto Market Fit Is Different

Call this capitalism or entrepreneurship, but fighting for PMF is like playing capture the flag.

In web2, PMF is incredibly rare to find and even harder to maintain once you’ve found the promised land. But if you’ve ever found PMF, you know that waking up every morning means opening up your laptop and discovering a new competitor wants to kill you.

In our next Crypto Market Fit essay, we’ll analyze crypto and web3 projects that have shown signs of early PMF, many of which have had extraordinary financial outcomes for founders and investors.

We’ll then ask ourselves whether their early success, and more often their subsequent downfall, can offer us a definition of CMF. We’ll discuss growth tactics like tokens and airdrops and how they relate to CMF.

We’ll explore how the web3 premise of composability, interoperability, and community-led products means that maintaining crypto market fit is even harder after building a successful early web2 product.

Thank you Jamesin Seidel (Investor & Data Science at Chapter One) for your contributions to this research.

As a note, I haven’t sent a newsletter in awhile. My goal as always is to write more often, but whenever I promise that, I seem to slow down.

The content will mostly be about crypto, venture capital, and general tech musings.

The cadence will be more frequent than every few years, but I’m not committing to a schedule because life is pretty busy right now. I only send newsletters when I feel like the content is worth your time.

I’ve renamed the publication to “Crypto Journal” as a working title. If you want to unsubscribe, no hard feelings at all!